The random walk was mentioned

in the section on signals and noise as a type of

low-frequency ("pink") noise. Wikipedia says:

"A

random walk is a mathematical formalization of a path that

consists of a succession of random steps. For example, the path

traced by a molecule as it travels in a liquid or a gas, the

search path of a foraging animal, "superstring" behavior, the

price of a fluctuating stock and the financial status of a

gambler can all be modeled as random walks, although they may

not be truly random in reality."

Random walks describe and serve as a model for many kinds

of unstable behavior. Whereas white, 1/f, and blue noises are

anchored to a mean value to which they tend to return, random

walks tend to be more aimless and often drift off on one or

another direction, possibly never to return.  Mathematically, a

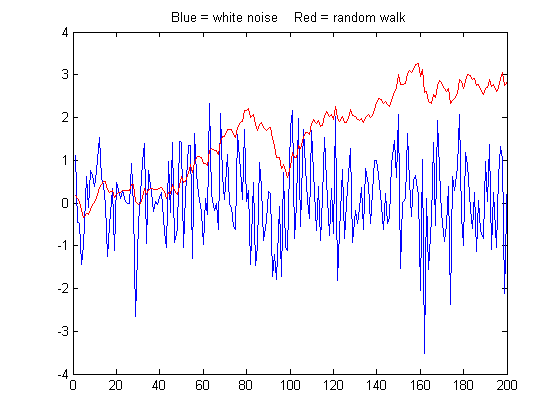

random walk can be modeled as the cumulative sum of some random

process, for example the 'randn' function. The graph on the

right compares a 200-point sample of white noise (computed as

'randn' and shown in blue) to a random

walk (computed as a cumulative sum, 'cumsum', and shown in red). Both samples are scaled to

have exactly the same standard deviation, but even so their behavior is vastly different. The

random walk has much more low frequency behavior, in this case

wandering off beyond the amplitude range of the white noise.

This type of random behavior is very disruptive to the

measurement process, distorting the shapes of peaks and causing

baselines to shift and making them hard to define, and it can

not be reduced significantly by smoothing (See NoiseColorTest.m).

In this particular example, the random walk has an overall

positive slope and a "bump" near the middle that could be

confused for a real signal peak (it's not; it's just noise). But

another sample might have very different

behavior. Unfortunately, it is not

uncommon to observe this behavior in experimental signals.

Mathematically, a

random walk can be modeled as the cumulative sum of some random

process, for example the 'randn' function. The graph on the

right compares a 200-point sample of white noise (computed as

'randn' and shown in blue) to a random

walk (computed as a cumulative sum, 'cumsum', and shown in red). Both samples are scaled to

have exactly the same standard deviation, but even so their behavior is vastly different. The

random walk has much more low frequency behavior, in this case

wandering off beyond the amplitude range of the white noise.

This type of random behavior is very disruptive to the

measurement process, distorting the shapes of peaks and causing

baselines to shift and making them hard to define, and it can

not be reduced significantly by smoothing (See NoiseColorTest.m).

In this particular example, the random walk has an overall

positive slope and a "bump" near the middle that could be

confused for a real signal peak (it's not; it's just noise). But

another sample might have very different

behavior. Unfortunately, it is not

uncommon to observe this behavior in experimental signals.

To demonstrate the measurement difficulties, the script RandomWalkBaseline.m

simulates a Gaussian peak with randomly variable position and

width, on a random walk baseline, with a S/N ratio is 15. The

peak is measured by least-squares curve fitting methods using peakfit.m with two

different methods of baseline correction in an attempt to handle

the random walk:

(a) a single-component Gaussian model (shape 1) with autozero set to 1 (meaning a linear baseline is first interpolated from the edges of the data segment and subtracted from the signal): peakfit([x;y],0,0,1,1,0,10,1);

(b) a 2-component model, the first being a Gaussian (shape 1) and the second a linear slope (shape 26), with autozero set to 1: peakfit([x;y],0,0,2,[1 26],[0 0],10,0).

In this particular case the fitting error is lower for the second method, especially if the peak falls near the edges of the data range.

But the

relative percent errors of the peak parameters show that the first method gives a

lower error for position and width, at least in this case. On

average, the peak parameters are about the same.

Position Error

Height Error Width Error

Method a: 0.2772

3.0306 0.0125

Method b: 0.4938

2.3085 1.5418

You can compare this to WhiteNoiseBaseline.m

which has a similar signal and S/N ratio, except that the noise

is white.

Interestingly, the fitting error

with white noise is greater, but the parameter errors (peak position,

height, width, and area) are lower, and the residuals are more random and less likely to

produce false noise peaks. This is because the random walk noise

is very highly concentrated at low frequencies where

the signal frequencies usually lie, whereas white noise also has

considerable power at higher

frequencies, which increases the fitting error but does comparatively little damage to signal

measurement accuracy. This may be slightly counter-intuitive,

but it's important to realize that fitting error does not always

correlate with peak parameter error. Bottom line: random

walk is troublesome.

Depending on the type of experiment, an instrumental design

based on modulation techniques may help, and

ensemble averaging multiple

measurements can help with any type of unpredictable random

noise, which is discussed in the very next section.

This page is part of "A Pragmatic Introduction to Signal

Processing", created and maintained by Prof. Tom O'Haver ,

Department of Chemistry and Biochemistry, The University of

Maryland at College Park. Comments, suggestions and questions

should be directed to Prof. O'Haver at toh@umd.edu. Updated July, 2022.

{kind=link}

{kind=link}